Heavy Duty Truck Aftermarket Outlook 2026 | Trends, Growth & Challenges | OURI

Jul 14 , 2026

Jul 14 , 2026If you operate in the heavy-duty truck aftermarket—whether as a fleet manager, a parts distributor, or a repair network owner—you have likely felt the whiplash of the past few years. A freight recession that refused to end. Tariffs that appeared without warning. Customers who postponed maintenance, then suddenly needed parts yesterday. The industry entered 2025 with muted expectations and ended the year with a market that many described as “solid, yet unspectacular”. Now, as 2026 unfolds, the question on everyone's mind is: what comes next?

This outlook examines the forces shaping the heavy-duty aftermarket in 2026—from growth drivers like an aging fleet population to headwinds like tariff volatility and technological disruption. Whether you are planning inventory, evaluating supplier relationships, or positioning your business for the year ahead, this guide provides the decision framework you need.

The 2026 Market at a Glance: Growth Despite Headwinds

The heavy-duty aftermarket in 2026 presents a paradox: the market is growing, but the growth is not coming from the usual sources. New truck sales remain depressed, yet aftermarket revenues are rising. Understanding this dynamic is the first step to navigating the year ahead.

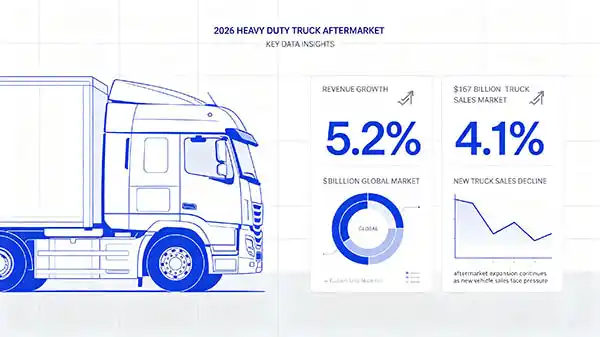

New truck sales are down, but the fleet is aging. In 2025, global sales of new medium- and heavy-duty trucks declined by approximately 4.1% compared to 2024. Early order-cycle indicators for 2026 suggest the industry is down another 20% year-over-year. Higher vehicle prices, tighter financing conditions, and freight market volatility are prompting operators to retain vehicles longer. As a result, global vehicles-in-operation (VIO) is still forecast to grow by 1.6% in 2026.

Aftermarket revenues are climbing. Despite weaker new truck sales, global aftermarket revenues are forecast to increase by approximately 5.2% year-on-year in 2026, supported by extended fleet lifecycles and higher vehicle utilization rates. Frost & Sullivan projects global commercial vehicle aftermarket sales will reach $167 billion in 2026. Within North America alone, aftermarket revenue is expected to jump from $36.46 billion to $38.56 billion.

Regional variations matter. Asia-Pacific, North America, and Europe are the major revenue contributors, with Europe projected to be the fastest-growing region. Latin America is emerging as a standout, with medium- and heavy-duty vehicle aftermarket growth of 6.9% year-on-year, driven by nearshoring trends and expanding auto exports.

The bottom line: The aftermarket is not booming in the traditional sense—but it is growing steadily. For B2B buyers and suppliers alike, understanding where that growth is coming from is essential for making informed decisions.

To explore the range of components available for an aging fleet with diverse maintenance needs, you can review the comprehensive product catalog.

Key Growth Drivers — What's Fueling the Aftermarket in 2026

Several structural trends are driving aftermarket demand in 2026, independent of new truck sales cycles. These are not temporary spikes—they represent fundamental shifts in how trucks are operated and maintained.

1. An aging vehicle fleet. Truck fleets in Europe and North America are aging beyond 12 years. Older vehicles generate higher parts replacement frequency and maintenance intensity, sustaining long-term aftermarket demand. As one industry observer noted, “a larger, older fleet translates directly into increased demand for repair, maintenance and personalization”. For parts suppliers and distributors, this means sustained demand for replacement components across almost every vehicle system.

2. Extended trade cycles and higher utilization. Facing economic uncertainty, fleets are stretching trade cycles—keeping trucks on the road longer and driving them harder. Higher vehicle utilization rates mean more wear and tear, which translates into more frequent parts replacement. As Daimler Truck North America's aftermarket senior vice president noted, customers “can't defy gravity for long”—eventually, deferred maintenance must be addressed.

3. The technician shortage. A global technician shortage is pushing workshops toward digital diagnostics, remote technical support, and structured training ecosystems. This shortage is not just a labor issue—it is reshaping how parts are sourced, diagnosed, and installed. Shops with fewer skilled technicians are increasingly relying on suppliers who can provide not just parts, but also the data and support needed to install them correctly.

4. Growing acceptance of aftermarket and private-label parts. As trucks age and cost pressures mount, sourcing is shifting from OEM dealers to heavy-duty distributors and independent garages. MacKay & Company reports that engine distributors and auto parts stores are seeing increased adoption of aftermarket and non-OE parts in 2025 compared to prior years. Industry leaders agree that private label is “no longer fringe”—quality has improved, customer acceptance has increased, and it is now a standard part of the purchasing mix.

The Major Challenges Facing the 2026 Aftermarket

Growth does not mean smooth sailing. The 2026 aftermarket faces significant headwinds that are reshaping how businesses operate and compete.

Tariff volatility and cost pressure. Counter-tariffs and trade tensions—primarily U.S. tariffs on imported trucks and parts—are increasing cost pressures, creating supply volatility, and compressing margins across the aftermarket value chain. Tariff-related price inflation drove most independent aftermarket growth across the United States and Canada in 2025, with price accounting for 4.0% of last year's 5.0% growth. As DTNA's aftermarket leader observed, tariffs are “sticky”—once implemented, they are difficult to reverse. “Unlike other regulatory measures, tariffs don't impact all OEMs and all suppliers equally,” he noted. “They vary by product footprint”.

The lingering freight recession. Despite a relatively healthy broader economy, fleets continue to face freight softness, excess capacity, higher borrowing costs, inflation, and uncertainty. The freight recession is not impacting aftermarket entities as directly as their dealer counterparts, but it is still limiting their growth potential. Until macroeconomic factors change course and reinvigorate carrier investment, competition will remain fierce and growth opportunities limited.

A “wait-and-see” mindset. Perhaps the most pervasive challenge is psychological. As one industry executive put it, “The single hardest part of 2025 [was] the pervasive 'wait-and-see' mindset across fleets, manufacturers and end-users. When capital expenditure is uncertain—whether for new truck orders, fleet investments or parts purchases—decision-making gets delayed”. This cautious approach is expected to persist into 2026, with most industry leaders adopting a “cautiously optimistic” outlook—expecting conditions to improve, but slowly.

Electrification complexity. Government electrification mandates are tightening across North America and Europe. Fleet operators seeking lower operational costs are adopting EVs faster than aftermarket service providers can scale expertise. EV maintenance fundamentally differs from traditional internal combustion engine service, eliminating entire service categories while creating new ones. Aftermarket providers are now investing in EV servicing capabilities, software diagnostics, ADAS calibration infrastructure, and connected service platforms. For traditional parts suppliers, this represents both a threat and an opportunity.

Five Strategic Shapes of the 2026 Aftermarket

Beyond the numbers and challenges, several deeper transformations are reshaping the competitive landscape.

1. From transactional to partnership-based relationships. Challenging conditions separate true partners from transactional ones. Industry leaders consistently report that tough environments reveal who communicates, collaborates, and follows through when complexity rises. The way suppliers behave during disruption is influencing how customers think about partnerships “this year and beyond”.

2. Digital transformation is accelerating. The aftermarket is no longer just about selling replacement parts. Digital platforms are redefining parts procurement and fleet management at scale. Companies are using AI to enable intelligent pricing, predict demand for spare parts, automate cash applications, and improve service planning. As one supplier executive noted, “We have to use advanced technology as a supplier to make that information available”—catalogs alone no longer suffice. Telematics and IoT integration are transforming maintenance from reactive breakdown response to proactive, connectivity-enabled health monitoring.

3. Supply chain restructuring. Driven by tariff volatility, sustainability mandates, and geopolitical risks, organizations are dismantling centralized, globalized supply networks in favor of regionally diversified models that prioritize flexibility, compliance, and customer alignment. North America is seeing nearshoring initiatives redirect supply chains to Mexico and Central America. Europe is building domestic supplier networks and strengthening partnerships with Eastern European manufacturers. Multi-source, geographically distributed supplier networks provide operational flexibility to absorb tariff changes, currency fluctuations, and regional demand shifts.

4. The rise of remanufacturing and circular economy. The remanufactured parts market is gaining traction—not just for cost savings, but for environmental sustainability. Remanufacturing is primarily onshore manufacturing, which also helps mitigate tariff exposure. Companies are investing in remanufactured component programs and circular economy practices that extend component lifecycles while reducing raw material dependency.

5. Value-aligned products for older trucks. With customers stretching trade cycles, OEMs are focusing more on value-aligned products typically more popular among owners of older trucks. This includes expanded private-label portfolios, bundled service offerings, and third-party warranty programs.

What This Means for B2B Buyers and Parts Distributors

For those sourcing truck parts in 2026, the outlook offers both challenges and opportunities.

For fleet operators and repair networks: The aging of your fleet means maintenance intensity will increase. Planning parts inventory around extended vehicle lifecycles—rather than new truck replacement cycles—is essential. The shift toward aftermarket and private-label parts means more options at different price points, but also requires careful supplier evaluation. Stronger supplier partnerships, built on communication and reliability, matter more than ever.

For parts distributors: The growth in aftermarket parts adoption presents a significant opportunity. However, tariff volatility means pricing and supply chains require constant monitoring. Digital capabilities—from AI-powered demand forecasting to integrated ordering platforms—are becoming competitive necessities rather than optional upgrades. Those who can provide not just parts but also data, support, and reliability will win in a market where customers are increasingly value-sensitive and digitally empowered.

For suppliers: The shift toward regional supply chains and value-aligned products means adapting product portfolios and distribution strategies. Investment in EV servicing capabilities and digital platforms is no longer optional. And perhaps most importantly, the way you communicate and collaborate during disruption will shape customer relationships for years to come.

Once you have clarified these key decision factors—such as your parts consumption patterns, the age profile of your fleet, and your tolerance for supply chain volatility—comparing the specific capabilities of available suppliers becomes the next logical step. You can review OURI's comprehensive product range for high-volume procurement scenarios or specialized component needs.

Related Reading

-

How to Streamline Your Truck Parts Procurement Process for Faster Turnaround

-

Is Outsourcing Your Truck Parts Supply Chain Cost Effective for B2B?

-

How to Source Heavy Duty Truck Parts from China: A Step-by-Step Guide

-

7 Most Commonly Overlooked Truck Maintenance Tasks You Shouldn't Ignore

This article is part of OURI's technical content library. No direct sales or pricing information is included. All technical discussions aim to help you make informed purchasing decisions.